Uber Ads: Accelerating the path to profitability

What makes advertising attractive is that it’s a 100% margin product that can subsidize the lower margin core business.

Earlier this week, Uber announced their first ever profitable quarter. Nelson Chai, Uber CFO, reported:

“The unique power of the Uber platform and the team’s relentless focus on profitable growth was on full display in Q2, with record profitability and over $1 billion of quarterly free cash flow.”

Uber’s stock has gone through a roller coaster journey since their IPO in 2019. Several factors contributed to this, including lower demand during COVID lockdowns, and a highly competitive market in both ridehailing and delivery. Uber’s stock was hit hard when the market correction began in 2022, particularly given their lack of profitability. So, their first profitable quarter is a remarkable milestone for the company.

One number stood out in their earnings. That was Uber ads’ annual revenue run rate — $650M. Even though the advertising business has only been around for four years, $650M (for simplicity, assume this is pure profit given advertising is an all-margin business) is ~15% of Uber’s annual free cash flow. Undeniably, this has been one of their largest drivers of profitability.

In this article, we’ll dive into:

- Uber’s difficult path to profitability

- Breaking out of the low profitability loop

- The Uber ads product

- How successful can this be

Uber’s difficult path to profitability

Since Uber’s founding in 2009, the ridehailing business has grown exponentially. An influx of venture capital money into the industry kicked off an era of heavily discounted rides and regulatory successes against taxi cartels, ending with Uber owning 70%+ of the US market today. The recent years also saw a steady state emerge in non-US geographies — Uber sold their China business for a partial stake in Didi and continued to maintain a 40–50% market share in India.

However, the market in most geographies today continues to be a duopoly, and Uber continues to have to engage in price wars given the lack of consumer loyalty towards a particular brand. In fact, despite getting to profitability this quarter, Uber’s stock dropped due to concerns about a re-emerging price war with Lyft.

In the delivery business, while UberEats had a first mover advantage, DoorDash now has the the lead in the US. While this business has grown steeply through the pandemic and now constitutes ~half of gross bookings, the market continues to be highly competitive, limiting how profitable Uber can be.

Breaking out of the low profitability loop

Uber has made some strategic product investments to break out of this loop, let’s look at a few.

They launched Uber One — a monthly subscription that provides $0 delivery fee on Uber Eats, ~5% discounts on Uber rides and promotions at specific restaurants. Uber says they have ~12M subscribers. On a generous basis, the $10/month subscription generates ~$1.4B in annual revenue, which could be very meaningful especially if it can make consumers use Uber more often. On a conservative basis, 12M is the current active subscribers at this moment on time but does not account for how many would churn. I would imagine that the churn rate is high + the acquisition rate is not great, given several competitor memberships come complimentary (Chase Sapphire gives you free DashPass, Amazon Prime gives you free GrubHub+). Nevertheless, even at a limited level of success, this could make a meaningful dent to profitability.

Uber also announced a multi-year partnership with Waymo to start bringing autonomous vehicles into the platform long-term. While this is likely to take a while to play out, it could be a long-term driver for profitability.

Uber mentioned another interesting win in their earnings press release but in suspiciously vague terms: “Mobility Revenue in Q2 2022 and Q2 2023 benefited from business model changes in the UK by $1.1 billion and $1.4 billion, respectively”. Upon further digging, it turns out that Uber started showing drivers how much they would earn while accepting a ride, instead of the total price of the ride. For example, Uber would show a driver that they would make 4 GBP instead of showing ride price as 5 GBP (of which Uber takes ~20%). This was done in response to new UK regulation, but the impact was surprising: “Mobility Take Rate in Q2 2022 and Q2 2023 includes a net benefit from business model changes in the UK of 810 bps in each period”. In other words, changes to how prices were shown to drivers created opacity, that effectively let Uber increase their take rates by ~8 percent points, thereby increasing Uber’s profitability.

Beyond these, the most notable profitability driver for them was advertising.

The Uber ads product

Uber has a few different product offerings tied to surfaces where ads can be shown. On the Uber Eats app:

- Sponsored Listings let restaurants appear in front of users when they’re deciding what to order, directly tying the ad to the success outcome of UberEats transactions

- Storefront Ads and In-Menu Ads allow promoting specific items within a restaurant / business’ list of items, typically catered towards consumer packaged goods advertisers (eg. PepsiCo promoting Doritos when you’re ordering from 7-Eleven)

- Post-Checkout Ads let any advertiser (doesn’t have be an Eats business) to show brand awareness ads, including video

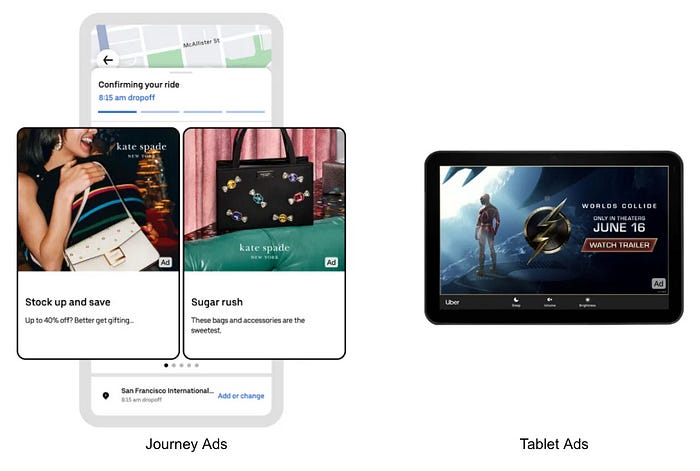

In the Uber ridehailing app, they offer Journey Ads (video or image ads that appear when you’re waiting for your or during your ride) and Tablet Ads (on Ubers that have tablets). These formats can be used by any advertiser but primarily work for brand awareness purposes.

What makes advertising attractive for Uber as a company is that it’s essentially a 100% margin product. Ridehailing and delivery are high scale but low-medium margin businesses — Uber typically keeps 20–30% of the gross bookings. With ads, Uber can create advertising inventory at zero cost and keep 100% of the revenue generated.

Advertising does not exist in a vacuum (i.e. if there are no users in the ridehailing and delivery apps, there is no ad inventory to monetize) but in the presence of high consumer engagement, it’s an incredibly powerful tool for Uber to generate net new profits that subsidizes the lower margin core business.

How successful can this be

The success of this product depends on being able to sell into a large set of advertisers and scale revenue. How much advertisers are willing to pay is typically determined by: scale of users, outcomes a particular surface / ad format can drive, ability to target specific users, and the ability to measure outcomes.

Uber definitely has the scale (137M monthly users). They also have robust data to target users based on a variety of factors — like loyalty to a restaurant, cuisine interest, past items purchased, locations visited, location trends, and more.

Among the ad surfaces, there is a clear duality. UberEats is a cleaner pitch for any performance advertiser — spend ad money with Uber and measure the value of UberEats transactions generated. The ROI is straightforward and given UberEats’ market share, this is an easy sell. However, ads within the Uber ridehailing app are a trickier sell. Uber makes the argument:

An average ride is about 20 minutes, which means 20 minutes where a person is leaned back and really receptive to advertising. And that’s where a lot of clients, such as those in entertainment, fashion, travel and financial, are using the opportunity to engage our consumers. The idea here is really to go into more CTV (connected TV) types of advertising campaigns. It’s basically your TV placement.

These placements are likely to work better when a brand is interested in building awareness — either for the brand itself (eg. the GEICO ad you see on TV) or for a particular seasonal product (eg. the ad you see on NYTimes when Nissan is releasing a new Rogue model). Typically, the placements that receive high cost per impressions (CPM) are the ones that are very high quality / have dedicated eyeballs (eg. SuperBowl ads) and are well-targeted, and Uber is only one of those.

Not to say this isn’t an opportunity — several advertisers have large branding budgets and Uber’s scale gives them a clear right to take a piece of the branding pie, and they will. What could further accelerate this opportunity is the creation of more formats that could cleanly tie to advertiser ROI — until then, I’m most bullish about UberEats ads and I am excited to see advertising be a key profitability driver for the company.

Thank you for reading! Liked this piece? Do consider subscribing to my weekly Substack newsletter. I publish one in-depth analysis of a current tech and business topic every week, in the form of a 10-minute read. Best, Viggy.